If you’ve been looking to buy a home lately, you already know—affordability is still one of the biggest challenges in today’s market.

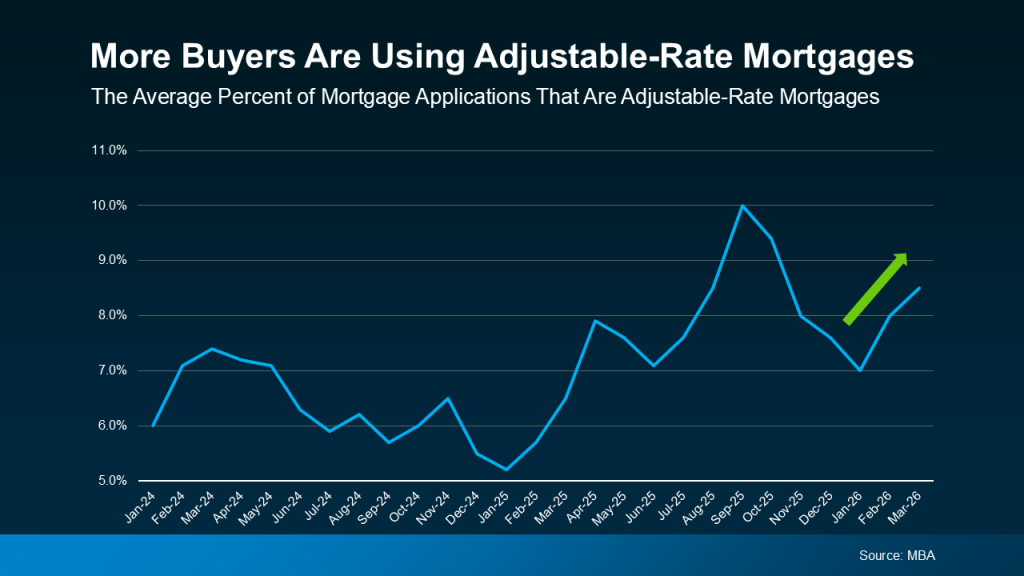

That’s exactly why more buyers are starting to consider something that wasn’t as popular before: adjustable-rate mortgages (ARMs).

But before you jump in, let’s break it down clearly—no complicated language, just what you actually need to know.

What Is an Adjustable-Rate Mortgage (ARM)?

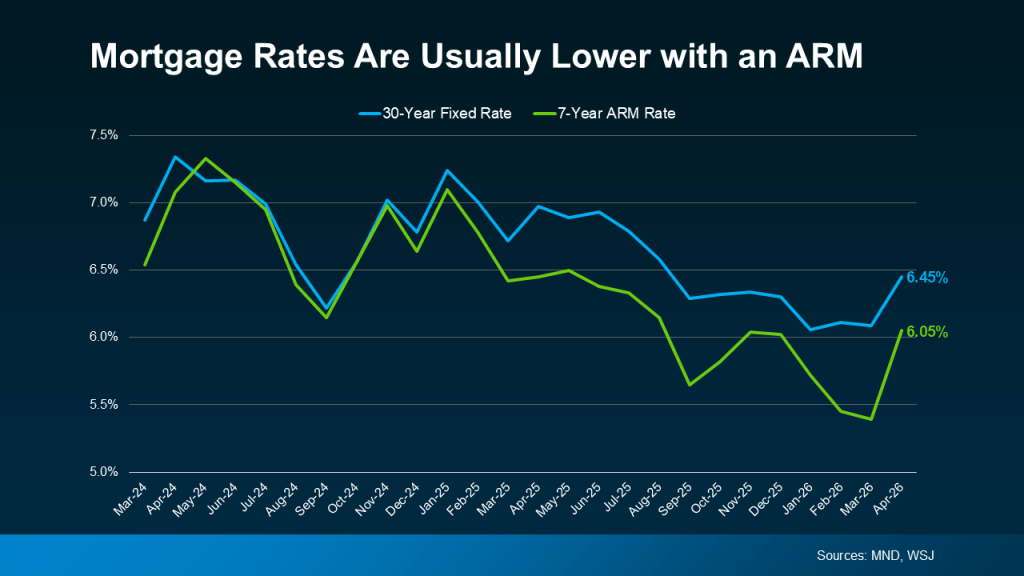

An adjustable-rate mortgage is a loan that starts with a fixed interest rate for a certain period (usually 3, 5, or 7 years). After that, the rate can change over time based on market conditions.

In simple terms:

- A fixed-rate mortgage = predictable, stable payments

- An ARM = lower starting payment, but it can change later

That means your monthly payment could go up… or down.

Why More Buyers Are Considering ARMs

Right now, many buyers are looking for ways to make homeownership more affordable—and this is where ARMs come into play.

Because ARM rates are typically lower at the beginning, they can:

- Lower your monthly payment

- Help you qualify for a higher-priced home

- Give you more flexibility in the short term

In fact, some estimates show buyers could save around $150 per month compared to a 30-year fixed mortgage.

And for many families, that difference matters.

Are ARMs Risky? Let’s Talk Realistically

A lot of people hear “adjustable-rate” and immediately think about the 2008 crash.

But here’s the truth:

Today’s lending standards are much stricter.

Lenders now evaluate whether you could still afford the loan even if rates increase.

So no—this isn’t the same situation as before.

What’s happening now is simply this:

Buyers are adapting to today’s market.

When an ARM Might Make Sense

An ARM can be a smart strategy if:

- You don’t plan to stay in the home long-term

- You expect your income to increase

- You’re planning to refinance before the rate adjusts

In these cases, you could take advantage of the lower initial rate without ever feeling the long-term impact.

The Trade-Off You Need To Understand

Here’s where you need to be honest with yourself.

Once the fixed period ends:

- Your interest rate can increase

- Your monthly payment can go up

- And there’s no guarantee rates will drop in the future

That means refinancing is not always a sure thing.

This is why strategy matters—not just the rate.

ARMs are getting more attention because they can make buying a home more affordable right now—but they’re not for everyone.

The key isn’t choosing the “cheapest” option.

It’s choosing the right strategy for your life and your plans.

Thinking about buying a home and not sure which financing option makes the most sense?

At Alzate Realty, we don’t just show you houses—we guide you through smart decisions that protect your future.

📲 Let’s talk. We’ll help you understand your options and connect you with Enrique Alzate, the right professional so you can move forward with confidence.