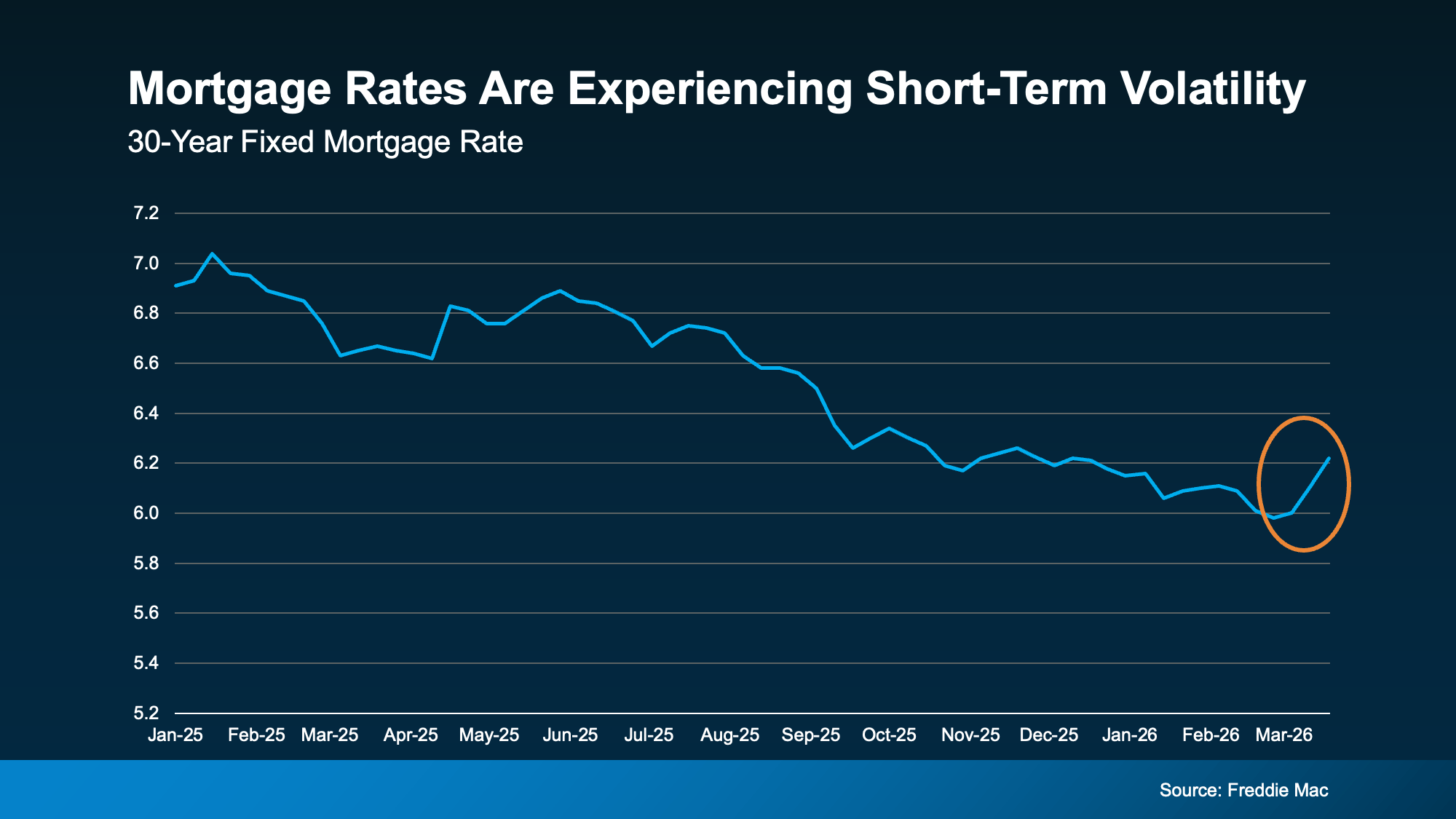

You Can’t Control Mortgage Rates… But You Can Control This

Mortgage rates are constantly changing, but that doesn’t mean you have to wait. Learn what you can control to buy smarter in today’s market.

Mortgage rates are constantly changing, but that doesn’t mean you have to wait. Learn what you can control to buy smarter in today’s market.

Many buyers are waiting for mortgage rates to drop before buying a home. But the actual difference in monthly payments may be smaller than expected. Here’s what buyers should really consider in today’s market.

Many renters assume buying a home is out of reach — but in many areas, owning is now more affordable than renting. Discover what the numbers really say, how local market conditions in Charlotte impact affordability, and whether homeownership may be more realistic than you think.

Housing inventory in Charlotte NC is increasing in 2026. Discover what this means for buyers and sellers and whether now is the right time to make a move.